In today’s competitive finance landscape, mastering basic accounting concepts stands as a cornerstone for career advancement. Whether you aspire to become an auditor, tax consultant, or financial analyst, these foundational elements equip you with the precision needed to interpret business health and drive informed decisions. This post delves into essential bookkeeping principles, starting with the double-entry system, key guiding principles, types of accounts, and preparation of financial statements. Professionals and students alike will discover how grasping these core accounting fundamentals unlocks opportunities in auditing, taxation, and beyond, particularly in dynamic markets like India where GST compliance demands meticulous transaction logging.

What Is the Double-Entry System in Basic Accounting Concepts?

The double-entry system forms the bedrock of basic accounting concepts, ensuring every financial transaction receives balanced recording across accounts. This method prevents errors and provides a complete audit trail, vital for career roles involving compliance and analysis. Originating centuries ago, it mandates that for every debit, a corresponding credit exists, maintaining the accounting equation’s integrity. In practice, businesses rely on it for accurate journal entries that feed into ledgers and trial balances.

Accountants use this system daily to log transactions like sales or purchases, fostering reliability in financial reporting.

- Each transaction affects at minimum two accounts, where debits equal credits.

- Debits increase assets or expenses; credits increase liabilities, revenue, or equity.

- For an Indian retailer recording a GST-inclusive sale of ₹10,000 (₹9,000 product + ₹1,000 GST), debit cash ₹10,000 and credit revenue ₹9,000 plus GST liability ₹1,000.

- Journal entries capture initial details, such as “Debit Accounts Receivable, Credit Sales Revenue.”

- Ledgers summarize postings from journals, enabling trial balance preparation to verify balance.

- Errors surface quickly if debits and credits mismatch, safeguarding against fraud.

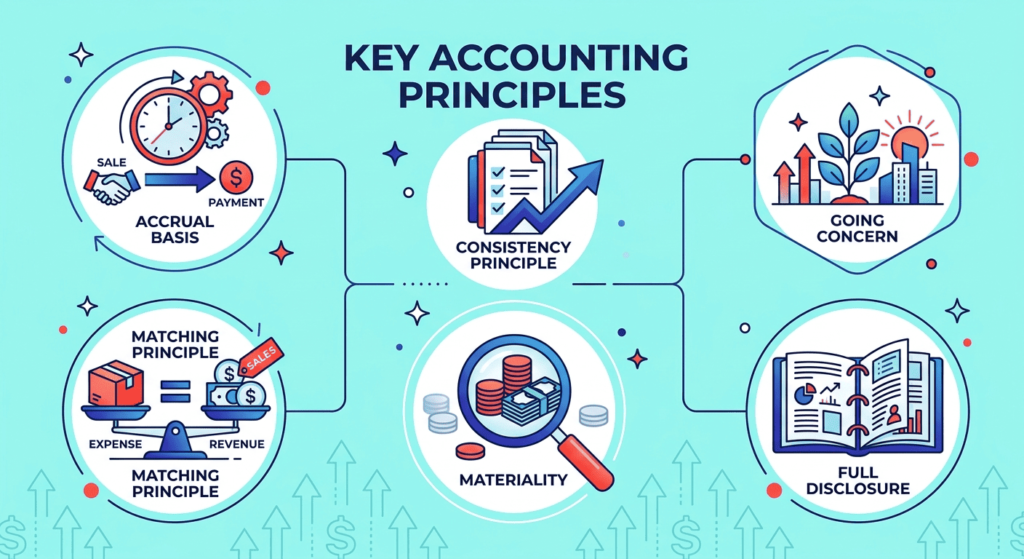

Key Accounting Principles That Guide Basic Accounting Concepts

Core accounting fundamentals rest on timeless principles that standardize practices worldwide, from GAAP in the U.S. to IFRS globally and Ind AS in India. These guidelines ensure consistency, comparability, and transparency in financial statements, empowering professionals to build trust with stakeholders. For instance, accrual basis recognizes revenue when earned, not received, contrasting cash basis for simpler tracking. Mastery here sharpens analytical skills essential for career progression in auditing or advisory roles.

These principles interconnect seamlessly, with going concern assuming business continuity and matching pairing expenses to revenues.

- Accrual Basis: Record revenues and expenses when they occur, not when cash changes hands; e.g., accrue salary expense at month-end.

- Consistency Principle: Apply the same methods year-over-year for comparable statements.

- Going Concern: Assume the entity operates indefinitely unless evidence suggests otherwise.

- Matching Principle: Align expenses with related revenues, like deducting cost of goods sold against sales.

- Materiality: Focus on information influencing decisions; minor transactions may use estimates.

- Full Disclosure: Reveal all relevant facts in notes to financial statements.

Types of Accounts in Basic Accounting Concepts

Understanding types of accounts anchors basic accounting concepts, classifying transactions into assets, liabilities, equity, revenue, and expenses for organized ledger management. This classification drives precise trial balance compilation and financial statement accuracy, a skillset demanded in finance careers for budgeting and forecasting. In India, businesses categorize GST payable under liabilities, highlighting real-world application.

Professionals categorize meticulously to reflect economic reality, ensuring debits and credits align per account rules.

- Assets: Resources owned, like cash, inventory, or accounts receivable; debits increase them.

- Liabilities: Obligations owed, such as loans or GST payable; credits increase them.

- Equity: Owner’s residual interest, including capital and retained earnings; credits boost it.

- Revenue: Inflows from operations, like sales; credits increase revenue accounts.

- Expenses: Outflows reducing equity, such as rent or salaries; debits raise them.

- Temporary accounts (revenue, expenses) close to permanent ones (equity) at period-end.

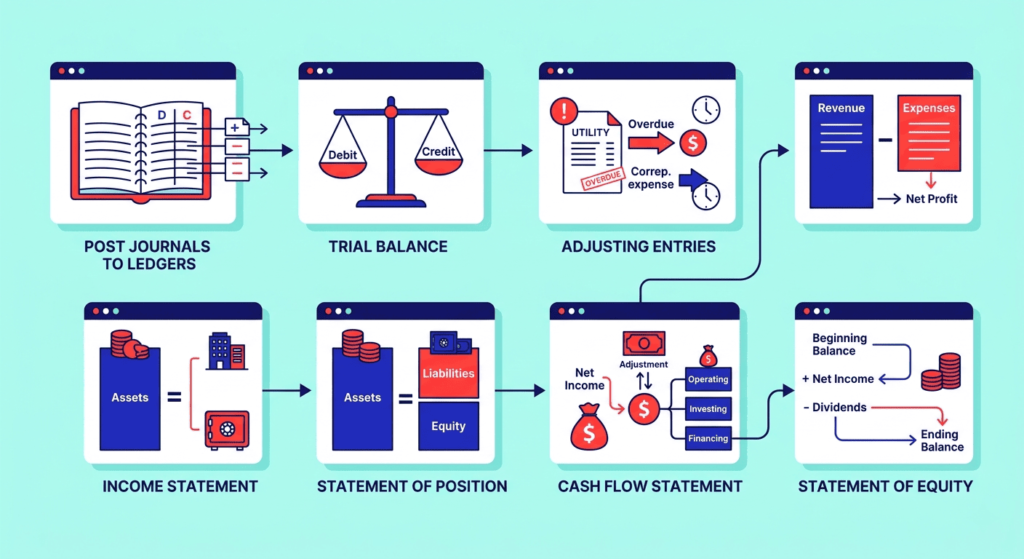

How to Prepare Financial Statements Using Basic Accounting Concepts

Financial statements emerge directly from basic accounting concepts, transforming journal entries and ledgers into balance sheets, income statements, cash flow statements, and statements of equity. This process builds topical authority in reporting, crucial for career success in analysis or compliance. Start with trial balance post-ledger postings, then adjust for accruals and prepare statements under GAAP or IFRS frameworks.

In India, incorporate GST impacts for accurate depiction, aiding stakeholders in assessing viability.

- Post journal entries to ledgers, then compile trial balance to confirm debits equal credits.

- Make adjusting entries for accruals, like unpaid utilities (debit expense, credit liability).

- Income statement shows revenues minus expenses for net profit, feeding retained earnings.

- Statement of position shows assets equal liabilities plus equity at a specific moment.

- Cash flow statement tracks operating, investing, financing activities under indirect method.

- Statement of equity reconciles beginning balance with net income, dividends, and ending figure.

Why Master Basic Accounting Concepts for Career Success?

Grasping basic accounting concepts propels professionals toward high-impact roles, from financial controller to forensic accountant, by enabling swift decision-making and regulatory adherence. In competitive fields, those fluent in essential bookkeeping principles excel in interpreting data amid complexities like IFRS transitions or GST audits. This foundation fosters adaptability, positioning you as indispensable in firms valuing precision.

Beyond technical prowess, it cultivates strategic thinking for career longevity.

- Enhances employability in auditing firms like the Big Four, demanding double-entry expertise.

- Supports taxation roles, accurately handling liabilities like GST or TDS.

- Boosts small business consulting, advising on cash vs. accrual basis choices.

- Prepares for certifications like CA or CPA, building on core fundamentals.

- Improves investor pitches by articulating balance sheet strengths.

- Drives promotions through error-free financial modeling and forecasting.

Conclusion

Mastering basic accounting concepts through an accounting course delivers transformative benefits, from error-proof transaction handling to insightful financial analysis that propels career trajectories in accounting and finance. These core accounting fundamentals double-entry precision, guiding principles, account classifications, and statement preparation interlink to form a robust framework, adaptable to global standards like IFRS or local nuances such as GST recording in India. Aspiring auditors gain audit trail confidence, tax experts streamline compliance, and analysts forecast with authority, unlocking doors to leadership in dynamic sectors.

Embrace these essentials today to stand out; practice by journaling sample transactions from a fictional Indian startup, reconciling to trial balance and statements. Consistent application sharpens skills, turning theoretical knowledge into career capital. Start your journey now your future in finance awaits those who act decisively.

FAQs

What are the most important basic accounting concepts for beginners?

- Double-entry system ensures balanced recording of every transaction.

- Accounting equation (Assets = Liabilities + Equity) underpins all basics.

- Key principles like accrual basis and matching guide accurate reporting.

- Types of accounts classify elements into assets, liabilities, revenue, expenses.

- Trial balance verifies ledger accuracy before statements.

How does the accounting equation relate to basic accounting concepts?

- It balances every transaction, central to double-entry in basic accounting concepts.

- Assets increase via debits; liabilities/equity via credits maintain equality.

- Impacts financial statements, like net income boosting equity.

- Applies universally, including GST liabilities in Indian ledgers.

- Violations signal errors, prompting journal reviews.

Can basic accounting concepts help in small business management in India?

- Double-entry tracks GST inputs/outputs precisely for compliance.

- Accrual basis reveals true profitability beyond cash flows.

- Account types aid budgeting, separating assets from expenses.

- Trial balance and statements support loan applications.

- Principles ensure consistency for growth audits.

What advanced topics build on basic accounting concepts?

- Managerial accounting for cost-volume-profit analysis.

- Auditing standards extending trial balance scrutiny.

- Tax computations layering GST onto income statements.

- IFRS convergence refining accrual applications.

- Forensic accounting probing ledger anomalies.